If you’re shopping for a mortgage in New Hampshire, your credit score affects your mortgage rate and has a bigger impact on your rate and costs than you might realize. Many borrowers assume loans are the same, but the truth is more nuanced—especially when it comes to how conventional loans and FHA loans treat credit scores differently.

Understanding how your credit score affects your mortgage rate can help you make smarter decisions about which loan program to choose and whether it makes sense to work on improving your score before you apply.

Let me walk you through exactly how this works.

How Conventional Loans Price Based on Credit Score

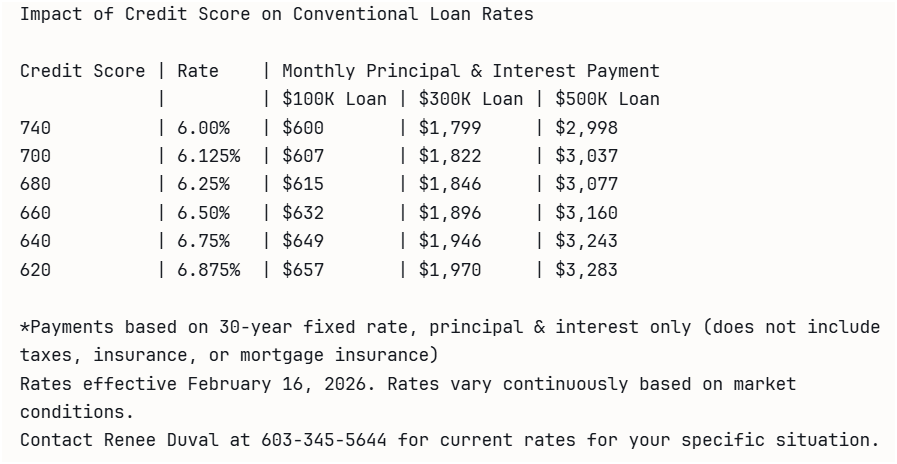

Conventional loans use something called “risk-based pricing.” This means that borrowers with lower credit scores are seen as higher risk, so lenders charge them higher interestInterest: the cost of borrowing money, charged as a percentage of the outstanding balance and paid in arrears (unlike rent, which is paid in advance). More rates to offset that risk.

Here’s what that looks like in practice: a borrower with a 740 credit score might get a 6% interestInterest: the cost of borrowing money, charged as a percentage of the outstanding balance and paid in arrears (unlike rent, which is paid in advance). More rate, while a borrower with a 640 credit score might get a 6.875% rate on the exact same loan amount with the same down payment.

The difference isn’t small. On a $300,000 loan, that 0.875% rate difference costs you about $170 more per month—or roughly $61,560 over the life of a 30-year mortgage.

Your credit score directly impacts your rate. The lower your score, the higher your rate.

Have a Lower Score But Still Want the Lower Rate?

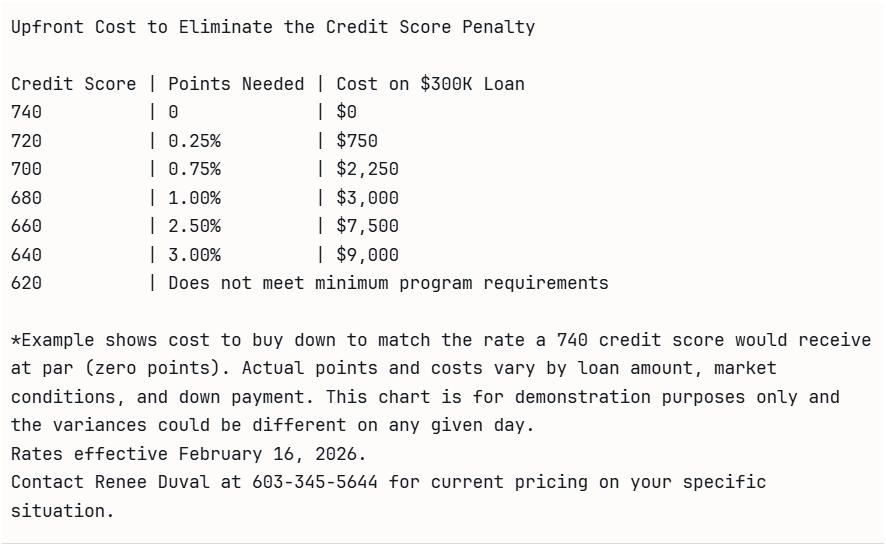

There’s another way conventional loans handle lower credit scores: instead of accepting a higher interestInterest: the cost of borrowing money, charged as a percentage of the outstanding balance and paid in arrears (unlike rent, which is paid in advance). More rate, you can pay “points” upfront to buy down your rate to match what a higher credit score would get.

One point equals 1% of your loan amount. So on a $300,000 loan, one point costs $3,000.

Here’s what that looks like: if you have a 680 credit score but want the same rate as someone with a 740 score, you’d need to pay 1% ($3,000) upfront at closingClosing is the meeting — typically in person — where all parties sign the final loan and property paperwork and the transaction becomes official. It’s the last step in the process, the point where months of paperwork, verification, and waiting turn into... More to buy down that rate.

The trade-off is simple: pay more upfront to lower your monthly payment, or accept a higher rate and keep your cash.

FHA Loans Take a Different Approach

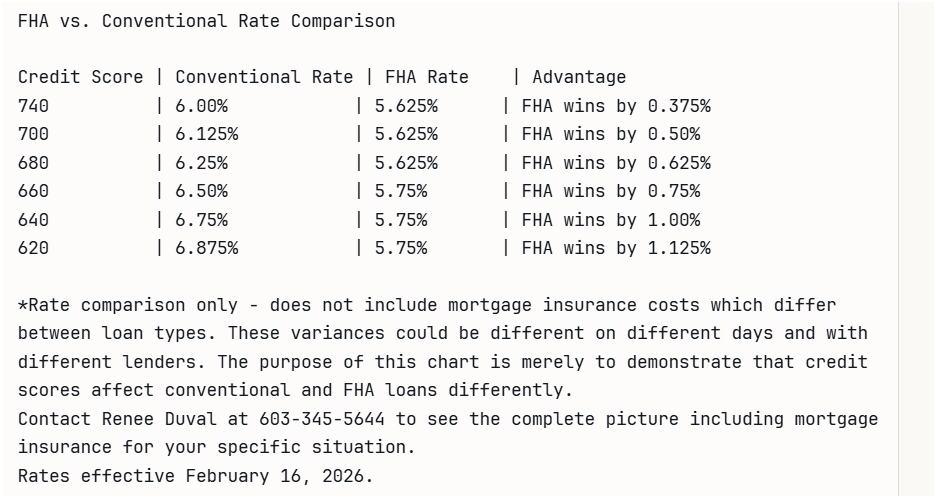

Unlike conventional loans, FHA loans don’t penalize lower credit scores nearly as much when it comes to interestInterest: the cost of borrowing money, charged as a percentage of the outstanding balance and paid in arrears (unlike rent, which is paid in advance). More rates.

FHA rates are more consistent across different credit scores. A borrower with a 740 credit score and a borrower with a 640 credit score might get rates that are only 0.125% to 0.25% apart—compared to the 0.75% to 1.00% difference you’d see with conventional loans.

This happens because FHA doesn’t use the same risk-based pricing model. The program was designed to help more people qualify for homeownership, so the rate structure is more forgiving for borrowers with lower credit scores.

Let me show you what this looks like in practice.

What Does This Mean for Your Mortgage Decision?

If you have a credit score below 740, FHA may deliver a better interestInterest: the cost of borrowing money, charged as a percentage of the outstanding balance and paid in arrears (unlike rent, which is paid in advance). More rate than conventional financing—sometimes significantly better.

A borrower with a 640 credit score could save on their monthly payment by choosing FHA over conventional, even after adding in the mortgage insurance costs.

But remember when deciding which mortgage program to go with, credit score, down payment, property type, property condition standards, and debt-to-income ratios all play a role in determining which loan program works best for your situation.

The only way to know for sure which program saves you the most money is to run the numbers on your specific situation. Want to start figuring this out for yourself? Get a quote here with minimal information, or call me at 603-345-5644 to talk through your specific situation. The choice is yours, and my goal is to help you choose wisely.

Ready to Explore Your Options?

Bookend Lending LLC is a New Hampshire-based independent mortgage broker focused on helping homeowners and homebuyers in NH find the best terms for their home mortgages. Whether you’re a first-time buyer in Manchester, refinancing in Portsmouth, or purchasing your next home anywhere in the Granite State, I’m here to help you navigate your options.

Learn More About Your Mortgage Options:

- Complete Guide to FHA Loans in New Hampshire

- Conventional Loan Requirements and Options

- First-Time Home Buyer Resources

- Understanding Credit Reports and Credit Scores

Questions? Call Renee Duval at 603-345-5644 or request a quote.