Every homeowner, homebuyer, and resident of New Hampshire is asking the same question this week: Will the Fed cut rates and will mortgage rates go down? Let’s walk through this story —like we’re summarizing a book.

How Fed Cuts Influence Mortgage Rates

The Federal Reserve (the Fed) sets a short-term interest rate called the federal funds rate – literally an overnight rate the rate banks charge each other for overnight loans. Mortgage rates are influenced by the Fed, but they’re not the same as what you’d pay on a new 30-year mortgage.

Mortgage rates follow the bond market, especially the 10-year Treasury bond, because most mortgages are bundled and sold as bonds tied to the 10-year Treasury yield.

So, when the Fed signals a possible cut, investors expect rates on the 10-year Treasury bond to drop nearly immediately and that can push mortgage rates down—but not always right away.

What’s Going On Right Now

At the Jackson Hole Economic Policy Symposium, held August 21-23, 2025, Fed Chair Jerome Powell hinted at a possible rate cut in September by pointing out weaknesses in the labor market and inflation risks. It was heavy with nuance rather than certainty – he didn’t confirm anything, but his message made markets sit up and pay attention. The response was quick: mortgage rates improved and the average 30‑year fixed rate dipped below 6.55%, which is the lowest we’ve seen this year (RealEstateNews.com).

Expert Forecasts

- From January through July 2025, the Fed has left rates unchanged.

- Analysts expect cuts in the 4th quarter of 2025

- In general, it’s believed there’s a 75–90% chance of a rate cut at the Fed’s mid-September meeting (Facebook, nhar-public.stats.showingtime.com, Politico).

- But remember—these are forecasts, not guarantees. Market sentiment can shift quickly depending on new data or events.

- Editor’s Note: If predicting rates were easy, I’d be a billionaire! The truth is, no one really knows.

Economic Indicators That Matter

Several signs help the Fed decide whether to cut rates—and influence the bond and mortgage markets:

- Jobs Data: If hiring slows or unemployment rises, it’s a hint the economy is softening and that could lead to lower rates to stimulate the economy.

- Inflation: If prices keep rising, the Fed might hold off on cutting.

What’s Happening in New Hampshire Real Estate

Here in NH, the housing market remains active—with slight price growth and more homes to choose from:

- Home sales are up 9% year-over-year, and prices rose 2.6%, with a median price around $512,800 in July (Steadily, Redfin).

- Inventory is increasing—an additional 15.9%, and median days on the market are around 34 days (Redfin).

- Homes are still selling fast—nearly 48% sold above asking price, although that’s slightly lower than last year (Redfin).

- According to New Hampshire Realtors, inventory for single-family homes increased over 28%, median sale price hit $545,000, and homes stayed on the market longer—about 21 days (nhar-public.stats.showingtime.com).

Advice for Homebuyers & Homeowners

- Life Timing Matters More Than Rate Timing

Getting married? Expecting a child? Downsizing? If the timing feels right, don’t let chasing a lower rate delay your big life move. - Get Preapproved Now

Even as you wait on rate direction, knowing your budget and rate options gives you confidence to move fast when the right home appears. - Watch, But Don’t Fear Rate Moves

Low rates are nice, but they can bounce around. If you’re ready, a 6% mortgage now is still better than waiting for a small cut when home prices may rise further.

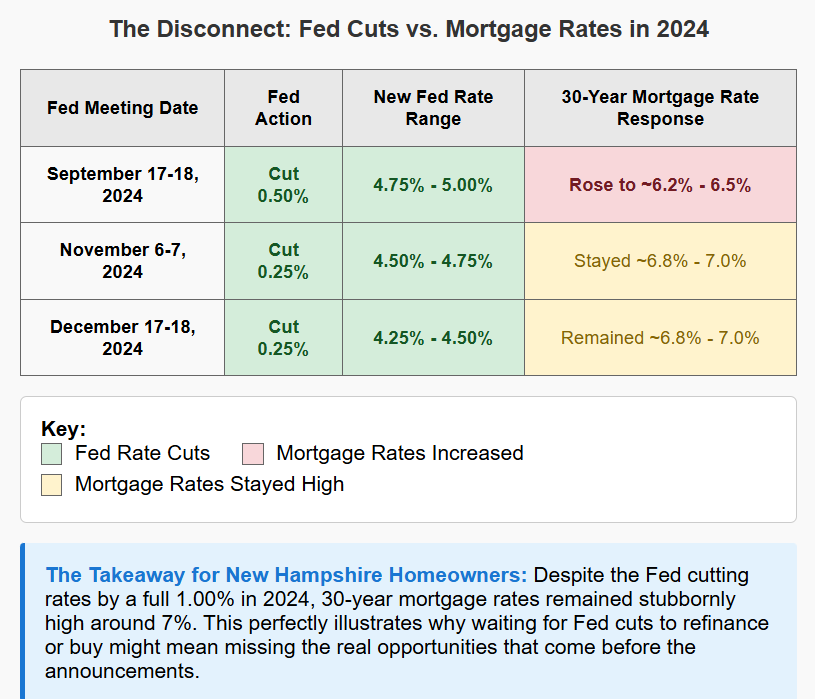

Why Mortgage Rates May Not Go Down Even If the Fed Cuts

It’s important to remember that a Fed cut doesn’t guarantee lower mortgage rates. Mortgage rates are influenced by many forces beyond the Fed’s decision:

- Mortgage-Backed Securities (MBS): Mortgage loans are bundled and sold as bonds – Mortgage-Backed Securities. When demand for these bonds is strong, rates tend to fall. When demand weakens, lenders raise rates to attract investors — even if the Fed is cutting short-term rates.

- Market Expectations: If the bond market has already anticipated a Fed cut, that expectation may already be “baked into” today’s mortgage rates. In other words, the market may have moved before the Fed ever announces.

- Political Pressure: If the Fed makes cuts due to political influence instead of pure economic data, markets may view the decision skeptically. That loss of confidence can push bond yields (and mortgage rates) higher.

- Global Factors: Mortgage rates also react to worldwide events — wars, trade tensions, oil prices, or shifts in global bond markets. Sometimes international news outweighs a Fed move in driving U.S. rates.

Bottom line: even with a Fed cut, mortgage rates can stay flat — or even rise — depending on how these other pieces of the puzzle play out.

Living in the Present

Living in the present matters — you can’t live your life in the future, making decisions based on what might happen. Some people want to wait for rates to drop before buying. Others buy now hoping they’ll refinance into a lower rate down the road. But refinancing isn’t guaranteed, and neither are lower rates. So don’t put your life on hold waiting for the “perfect” rate environment. When’s the best time to buy a home? Now! Now is the best time to buy a home if it’s the right time for you. Let Renee Duval and Bookend Lending LLC help you understand your options!

Final Thoughts

A Fed rate cut could help bring mortgage rates down over time—but timing the market is hard, and life waits for no one. If now is right for your family, home, or future plans, move forward with confidence. Preapprove, stay informed, and talk to a trusted mortgage professional who can help you navigate options—whether rates go down or hold steady.